Corporate fixed deposits are term deposits offered by companies and NBFCs to raise money from investors, while bank FDs are deposits accepted by banks from customers.

Corporate FDs usually offer higher interest rates than bank FDs, but they also carry higher risk because they are not covered by the same deposit insurance protection as bank FDs.

We will read in detail the key differences between corporate FDs and Bank FDs in this blog.

What Is a Corporate FD?

A corporate FD is a fixed deposit scheme offered by a company or NBFC for a fixed tenure at a fixed interest rate. These deposits are popular because they often offer better yields than regular bank FDs, especially when issued by high-rated companies.

Corporate FDs are generally used by issuers to raise capital for business purposes, and investors receive interest either at maturity or through periodic payouts depending on the chosen plan.

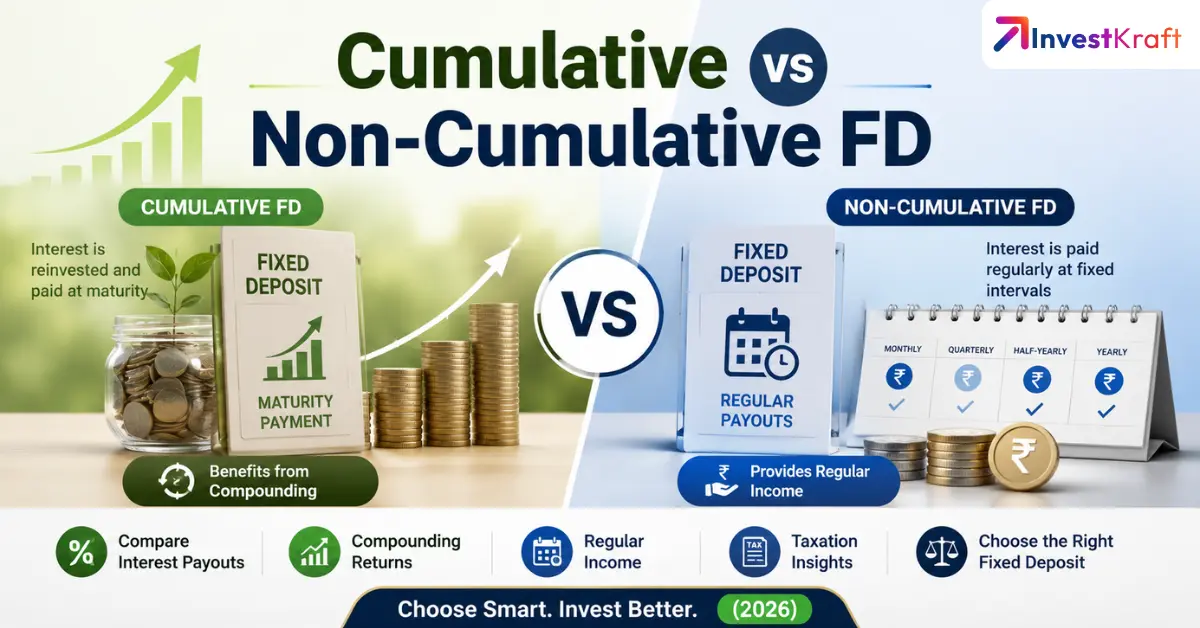

Many issuers offer both cumulative and non-cumulative options, so investors can choose between growth and regular income.

How Bank FDs Are Different

Bank FDs are deposits placed with scheduled banks, and they are usually considered safer because they come with DICGC insurance coverage up to ₹5 lakh per depositor per bank. This insurance makes bank FDs the more conservative choice for capital preservation.

Bank FDs also tend to have more uniform regulations and stronger liquidity confidence because they are part of the formal banking system.

Corporate FDs can still be good products, but the safety depends more on the issuer’s financial strength and credit rating.

Main Differences Between Corporate FD & Bank FD

The following are the main differences between corporate FD and Bank FD:

Feature

Corporate FD

Bank FD

Issuer

Company or NBFC

Bank

Interest rate

Usually higher, often around 1% to 3% more

Usually lower than corporate FDs

Safety

Depends on issuer and credit rating

Safer due to DICGC insurance up to ₹5 lakh

Insurance

No government-backed deposit insurance like bank FDs

DICGC protection up to ₹5 lakh per depositor per bank

Credit rating

Very important; AAA and AA ratings are preferred

Not typically compared the same way for deposit safety

Payout options

Cumulative and non-cumulative available

Also available in cumulative and non-cumulative forms

Premature withdrawal

Often allowed with penalty, or locked in for non-callable options

Usually allowed with penalty

Risk level

Higher than bank FD

Lower than corporate FD

Why Corporate FDs Offer Higher Returns

Corporate FDs generally pay more because investors are taking on more credit risk. Since the deposit is not backed by the same insurance protection as a bank FD, issuers compensate investors with better interest rates.

In practice, the spread can be meaningful for income-focused investors. Many corporate FDs quote rates in the 7% to 9% range depending on issuer quality, tenure, and payout structure.

FD Interest Rate Table: Banks vs Corporate / NBFC FDs

Now, let us compare the interest rates of Bank FDs and Corporate FDs from the table below:

Bank FDs

Bank / Institution

Approx. FD Interest Rate Range

Notes

Indian Bank

2.80% to 6.95% p.a.

Rates vary by tenure; senior citizens get an extra 0.50% p.a.

SBI

About 3.05% to 7.05% p.a.

Widely used benchmark bank FD range

ICICI Bank

About 2.75% to 7.10% p.a.

Rates vary by tenure and deposit amount

HDFC Bank

About 3.00% to 6.00%+ p.a.

Commonly seen among large private banks

Axis Bank

About 3.50% to 6.10% p.a.

Tenure-based rate structure

Kotak Mahindra Bank

About 3.00% to 5.60% p.a.

Lower end for shorter tenures

Bank of Baroda

About 3.50% to 5.70% p.a.

Public sector bank FD range

Punjab National Bank

About 3.50% to 5.75% p.a.

Public sector bank FD range

IDFC FIRST Bank

Up to about 7.40% p.a.

Higher-rate private bank among recent comparisons

Bandhan Bank

Up to about 7.40% p.a.

Often appears in higher-yield bank FD lists

Corporate / NBFC FDs

Corporate / NBFC

Approx. FD Interest Rate Range

Notes

Shriram Finance

About 7.00% to 8.10% p.a.

Higher-yield NBFC FD option +1

Muthoot Capital Services

Up to about 8.50% p.a.

Among the highest-yielding NBFC FDs mentioned recently

Sundaram Finance

About 7.50% to 8.00% p.a.

Popular corporate FD issuer

Bajaj Finance

About 6.70% to 7.30% p.a.

Large NBFC with widely tracked rates

ICICI Home Finance

About 6.70% to 7.30% p.a.

Corporate/NBFC-style deposit product

LIC Housing Finance

About 6.70% to 7.30% p.a.

Lower than the very top NBFC rates, but still above many bank FDs

Shivalik Small Finance Bank

Up to about 8.30% p.a.

High-rate deposit option in the recent comparison list

Slice Small Finance Bank

Up to about 7.75% p.a.

Deposit range in recent comparison list

Safety and Credit Rating

The most important factor in a corporate FD is the issuer’s credit rating.

AAA and AA-rated issuers are generally preferred because they indicate stronger repayment ability and lower default risk.

Investors should be extra careful with lower-rated issuers, even if the rate looks attractive. A slightly higher return does not always justify a weaker balance sheet or lower repayment comfort.

Tax and TDS Rules

Interest earned from corporate FDs is fully taxable under income tax rules, just like interest from bank FDs.

However, one important difference is that corporate FD interest is often subject to TDS once interest from a single company crosses ₹5,000 in a financial year.

The overview also notes that Form 15G/15H may not work in the same way for avoiding TDS on corporate FDs as it does with bank deposits.

That makes tax planning important, especially for investors who rely on periodic payout products.

Which FD Should You Choose?

Corporate FDs may suit investors who want higher returns and are comfortable evaluating credit quality.

They are often better for people who can lock money away and want to earn more than what standard bank FDs usually pay.

Bank FDs are better for conservative investors, emergency funds, and anyone who values deposit insurance and higher comfort over extra yield.

For many investors, a mix of both can be a practical way to balance return and safety.

A corporate FD is a fixed deposit offered by a company or NBFC to raise funds from investors at a fixed interest rate.

Are corporate FDs safe?

They can be safe if the issuer has a strong credit rating, but they are riskier than bank FDs because they do not have DICGC insurance.

Why do corporate FDs pay higher interest?

They usually pay more because investors take on more credit risk compared with bank FDs.

Do corporate FDs have insurance like bank FDs?

No, corporate FDs do not carry the same government-backed insurance protection that bank FDs get through DICGC.

Which corporate FD ratings are considered better?

AAA and AA-rated corporate FDs are generally preferred because they indicate lower credit risk.

Is corporate FD interest taxable?

Yes, interest from corporate FDs is fully taxable as income from other sources.

Should I choose a corporate FD or a bank FD?

Choose a corporate FD for higher returns if you are comfortable with more risk, and a bank FD if safety and insurance matter more.

Sources

Ujjivan Small Finance Bank: Corporate FDs vs Bank FDs

Groww: Differences between Corporate Fixed Deposit and Bank FD

Airtel Finance: Corporate FD vs Bank FD

Paisabazaar: Corporate Fixed Deposits

Nivesh: Company Fixed Deposit vs Bank Fixed Deposit

ET Money: Corporate Fixed Deposit

Disclaimer

This article is for general informational purposes only and should not be treated as financial, tax, or investment advice. Corporate FD interest rates, credit ratings, payout rules, tax treatment, and premature withdrawal penalties can change depending on the issuer and the prevailing regulations. Please verify the latest terms with the issuer or a qualified financial advisor before investing.

Author: Diwakar Kumar Singh

Diwakar Kumar Singh is a BFSI specialist and finance writer with over 7 years of hands-on experience in financial research, content creation, and analysis.

A Gold Medalist in MBA (Marketing) from IMT, he combines deep analytical skills with practical insights gained from evaluating companies, IPOs, unlisted shares, financial ratios, and investment opportunities. Diwakar has personally analysed hundreds of financial instruments and market scenarios, which he uses to break down complex topics into clear, actionable advice.

He has authored numerous in-depth finance articles, published multiple books internationally, and contributed to research publications. His work focuses on helping everyday investors and readers make better-informed financial decisions through well-researched, evidence-based explanations that are always grounded in real-world application rather than theory alone.