Fixed deposits (FDs) are one of the most popular investment options in India, offering safety and predictable returns. However, many investors get confused when choosing between cumulative and non-cumulative FDs. The key difference lies in how interest is paid out and reinvested, which directly impacts your total returns and cash flow.

Let us understand in detail what the key differences are.

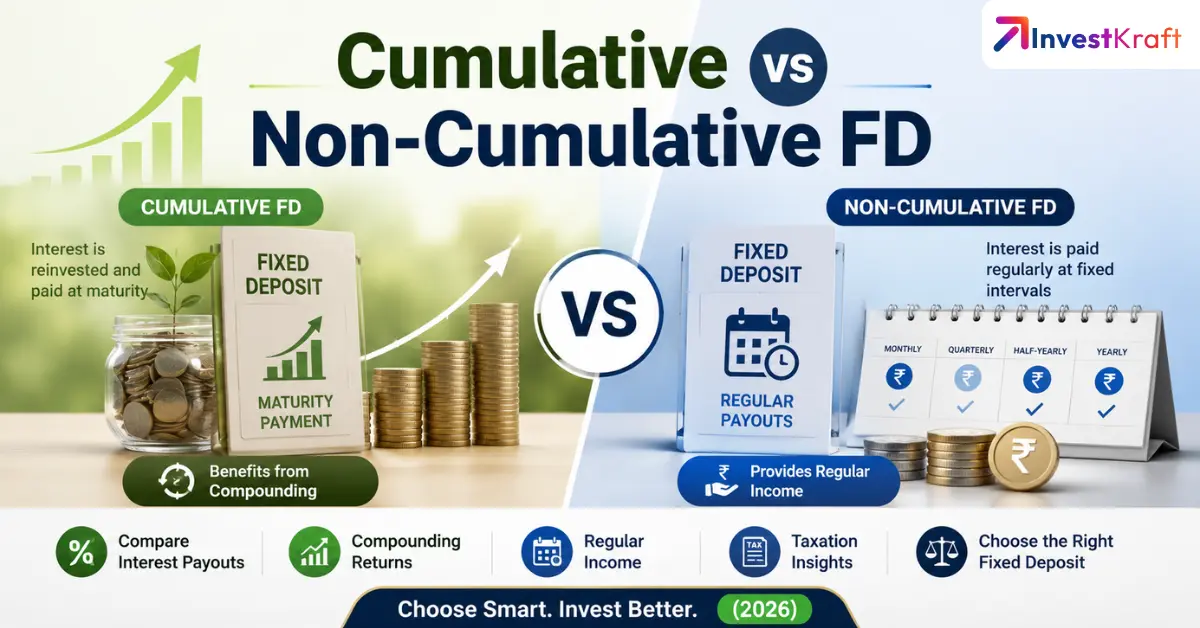

What is a Cumulative Fixed Deposit?

The word "cumulative" means accumulation. In a cumulative fixed deposit, the interest earned is accumulated throughout the FD tenure and paid out only at maturity.

How It Works:

Interest earned in each compounding period (annually or quarterly) is reinvested and added to the principal

This increases the principal amount, which in turn generates more interest

The power of compounding is fully utilised

At maturity, you receive the total amount: initial deposit & accumulated interest

Example: If you invest ₹1,00,000 in a Cumulative FD for 5 years at 7% p.a., you will earn approximately ₹41,478 as interest. At maturity, you receive ₹1,41,478 in total.

What is a Non-Cumulative Fixed Deposit?

A non-cumulative fixed deposit is where the accrued interest is paid regularly to the depositor instead of being accumulated.

How It Works:

Interest is paid out at pre-fixed frequencies: monthly, quarterly, half-yearly, or yearly

The principal amount remains static throughout the tenure

Interest is deposited directly into your bank account at each interval

Since interest is not reinvested, the compounding benefit is lost

Example: Using the same investment of ₹1,00,000 at 7% p.a. for 5 years with quarterly payout, you receive ₹1,750 every quarter (7% of ₹1,00,000 divided by 4). Over 5 years, total interest earned is ₹35,000

Key Differences Between Cumulative and Non-Cumulative FD

The following table highlights the important differences between cumulative and non-cumulative FD:

Particulars

Cumulative FD

Non-Cumulative FD

Definition

Interest accumulated throughout FD tenure

Interest not accumulated; paid regularly

Interest Payout

Paid entirely at maturity

Paid monthly, quarterly, half-yearly, or yearly

Income Flow

No income during tenure

Regular income throughout tenure

Reinvestment

Yes – interest earns interest

No – interest paid out, no reinvestment

Total Returns

Higher due to compounding power

Slightly lower – no compounding benefit

Cash Flow

Lump sum at maturity for large expenses

Regular income stream for ongoing expenses

Liquidity

Lower – funds accessible only at maturity

Higher – periodic payouts provide liquidity

Best Suited For

Salaried individuals, business owners

Retirees, pensioners, freelancers, homemakers

Investment Duration

Typically longer horizons

Short-term or long-term goals

Interest Payout Comparison

Now, let us see how interest calculation is done in both types of FDs.

Cumulative FD:

Paid entirely at maturity

Interest is compounded annually or quarterly and added to principal

Principal grows over time due to reinvestment

Non-Cumulative FD:

Paid out at regular intervals (monthly, quarterly, yearly)

Principal remains static; interest goes directly to bank account

No reinvestment option available

Which FD Type Offers Better Returns?

Now, let us see which FD offers better returns from the table below:

Aspect

Cumulative FD

Non-Cumulative FD

Total Returns

Yields higher returns due to compounding

Yields slightly lower returns

Earning Mechanism

Interest compounded annually/quarterly

Principal static; interest deposited directly

Why the Difference?

"Interest on interest" effect maximises returns

No compounding – interest not reinvested

Cumulative FDs yield higher total returns because of the compounding power, while non-cumulative FDs offer lower overall returns since interest is not reinvested.

Income Stream Comparison

Now, let us compare how the income stream varies in both the FDs from the table below:

Feature

Cumulative FD

Non-Cumulative FD

Income During Tenure

No income during deposit tenure

Regular, predictable income stream

Cash Flow Need

For those who don't need immediate cash flow

For those needing regular payout to cover expenses

Best For

Maximising long-term wealth

Retirees, pensioners, freelancers

Which FD Should You Choose?

Choose Cumulative FD If:

You are looking to maximise long-term wealth

You don't need immediate cash flow

You are a salaried individual or running a business

Your goal is to build a corpus for short- or long-term objectives

You want to multiply savings at an exponential rate

Choose Non-Cumulative FD If:

You need regular income for recurring expenses

You are a retiree, pensioner, or freelancer needing steady payouts

You are a homemaker seeking regular income

Your purpose is to add to existing income or provide pension after retirement

You depend on investments for day-to-day expenses

Remember: This is not an either-or decision. You can diversify your FD portfolio by investing in both types based on different financial goals.

Important Factors to Consider

The following are the important factors you need to consider before opening your FD account:

Factor

Cumulative FD

Non-Cumulative FD

Maturity Amount

Generally higher due to compounding

Principal remains constant

Liquidity

Lower – funds only at maturity

Higher – periodic payouts

Investment Horizon

Typically longer durations

Suitable for both short & long-term

Tax Implications

Interest taxed annually despite maturity payout

Interest taxed when received

Other Important Considerations:

1. Interest Rates

Cumulative FDs typically offer slightly higher interest rates due to compounding benefit

Non-cumulative FDs offer lower rates since compounding is not realized

2. Taxation

Cumulative FD: Interest is taxed annually even though you receive it at maturity

Non-Cumulative FD: Interest is taxed when you receive each payout

3. TDS (Tax Deducted at Source)

Banks deduct TDS if interest income exceeds ₹40,000/year (₹50,000 for seniors)

TDS rules apply differently based on payout frequency

How to Calculate Your Returns

You can use an FD Calculator to estimate returns for both types:

For Cumulative FD:

Enter:

Principal amount

Interest rate

Tenure

You will get the maturity amount and total interest earned.

For Non-Cumulative FD:

Same inputs, but select your preferred payout frequency (monthly/quarterly) to see periodic interest amounts.

Understanding the mechanics of cumulative and non-cumulative FDs helps you tailor your investment to your exact cash flow requirements. Cumulative FD for Wealth Maximisation: Best for long-term growth and corpus building

Non-Cumulative FD for Income Generation: Best for regular income needs and expense coverage

Frequently Asked Questions

What is the main difference between cumulative and non-cumulative fixed deposits?

In a cumulative FD, the interest is added back to the principal and paid at maturity. In a non-cumulative FD, interest is paid at regular intervals like monthly, quarterly, half-yearly, or yearly.

Which FD gives higher returns?

A cumulative FD usually gives higher total returns because the interest gets compounded during the tenure.

Who should choose a cumulative FD?

Cumulative FDs are better for investors who do not need regular income and want to build a larger corpus over time.

Who should choose a non-cumulative FD?

Non-cumulative FDs suit people who need periodic income, such as retirees, pensioners, or anyone who wants cash flow during the investment period.

Is the principal amount safe in both types of FD?

Yes, the principal remains fixed in both options. The difference is only in how interest is paid.

Are non-cumulative FDs useful for monthly expenses?

Yes, they are useful when you want a steady payout to cover regular expenses or supplement income.

Can I use an FD calculator to compare both options?

Yes, an FD calculator helps you estimate maturity value for cumulative FDs and periodic payout amounts for non-cumulative FDs.

Sources

Bajaj Finserv: Difference Between Cumulative and Non-Cumulative Fixed Deposit

Shriram Finance: Cumulative vs Non-Cumulative FD

Mahindra Finance: Difference Between Cumulative and Non-Cumulative FD Interest Rates

IDFC FIRST Bank: Cumulative vs Non-Cumulative FD

Paisabazaar: Cumulative vs Non-Cumulative FD

Axis Bank: Difference Between Cumulative & Non-Cumulative Fixed Deposits

Disclaimer

This article is for general informational purposes only and should not be considered financial, tax, or investment advice. FD interest rates, payout rules, and tax treatment may change based on the bank, tenure, deposit type, and prevailing regulations. Please verify current terms with the concerned bank or a qualified financial advisor before investing.

Author: Diwakar Kumar Singh

Diwakar Kumar Singh is a BFSI specialist and finance writer with over 7 years of hands-on experience in financial research, content creation, and analysis.

A Gold Medalist in MBA (Marketing) from IMT, he combines deep analytical skills with practical insights gained from evaluating companies, IPOs, unlisted shares, financial ratios, and investment opportunities. Diwakar has personally analysed hundreds of financial instruments and market scenarios, which he uses to break down complex topics into clear, actionable advice.

He has authored numerous in-depth finance articles, published multiple books internationally, and contributed to research publications. His work focuses on helping everyday investors and readers make better-informed financial decisions through well-researched, evidence-based explanations that are always grounded in real-world application rather than theory alone.