You are about to borrow ₹5 lakh at 12% per annum for 3 years. Your bank says your EMI is ₹16,607.

Should you trust that number? Where does it come from? And how much are you actually paying the bank in interest over the full tenure?

Understanding how personal loan interest is calculated is not just maths - it is power. The borrower who understands this can negotiate better rates, choose the right tenure, make smarter prepayments, and avoid being surprised by the total cost of their loan.

This guide covers everything: the EMI formula, step-by-step worked examples, flat rate vs reducing balance, amortisation schedules, and the free calculators every Indian borrower should bookmark. Before we proceed, let us take a look at the latest updates on personal loan interest calculations in 2026

Latest Highlights: Personal Loan Interest Calculation in 2026

As of June 2026, personal loan rates from 40+ banks and NBFCs in India range from 10% to 24% per annum on a reducing balance method. Higher risk profiles get higher rates - CIBIL score, income, employer category, city, job stability, and existing EMIs all factor in.

RBI mandates that all lenders must disclose the APR (Annual Percentage Rate) - including processing fees - in the Key Fact Statement. Always compare APR, not just the headline interest rate.

Nearly all personal loans in India now use the reducing balance method. Avoid flat-rate loans - they appear cheaper but cost significantly more overall.

InvestKraft now offers a free Personal Loan EMI Calculator at investkraft.com - enter any amount, rate, and tenure to instantly see your EMI, total interest, and year-by-year amortisation.

From January 2026, zero prepayment penalty on floating rate personal loans - understanding your amortisation schedule now helps you identify the best months to prepay and save maximum interest.

Two Methods of Calculating Interest - The One That Matters

Before the formula, you must understand which interest calculation method your lender uses:

Flat Rate Method

Interest is calculated on the original principal for the entire tenure - regardless of how much you have already repaid. This is expensive and misleading.

Formula: Total Interest = P × R × T Where P = Principal, R = Annual rate, T = Tenure in years

Reducing Balance Method (Most Common in India)

Most personal loans in India use the reducing balance method - interest is recalculated on the outstanding principal after each EMI payment.

As you repay principal each month, the interest charged in the next month reduces. This is fairer and cheaper than the flat rate method.

Real difference on ₹5 lakh loan at 12% for 3 years:

Method

Monthly EMI

Total Interest

What You Pay Extra

Flat Rate

₹18,889

₹1,80,000

₹82,148 more

Reducing Balance

₹16,607

₹97,852

(the right way)

Always confirm with your lender that the reducing balance method is being used. Fintech apps and some NBFCs sometimes advertise low flat rates that are deceptively expensive.

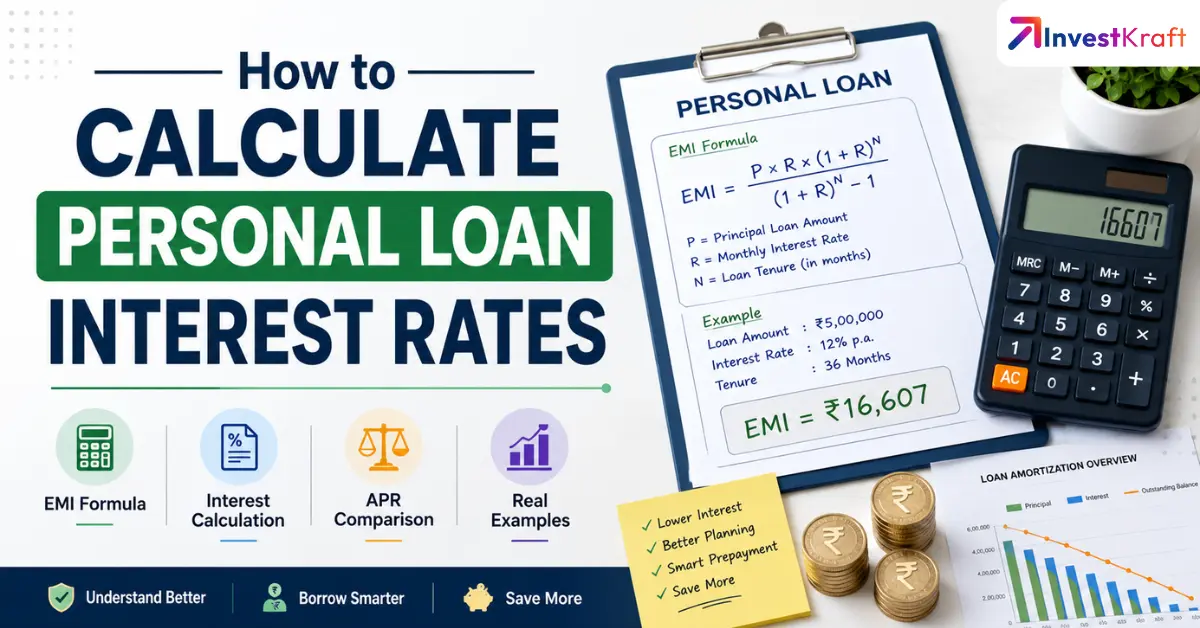

The EMI Formula - Explained Simply

The Equated Monthly Instalment (EMI) formula is:

EMI = P × R × (1 + R)^N ÷ [(1 + R)^N − 1]

Where: P = Principal loan amount (the amount you borrow) R = Monthly interest rate = Annual interest rate ÷ 12 ÷ 100 N = Loan tenure in months

This formula looks intimidating - but once you understand what each part does, it makes complete sense.

What does each part of the formula represent?

P × R = Your first month's interest charge (1 + R)^N = The compounding factor over the full tenure. The full formula balances the two so that each EMI is equal - a fixed amount - for the entire loan period, even though the split between interest and principal changes every month.

Step-by-Step Calculation - ₹5 Lakh at 12% for 3 Years

Given: P = ₹5,00,000 Annual interest rate = 12% per annum N = 3 years = 36 months

Step 1: Convert to monthly interest rate R = 12 ÷ 12 ÷ 100 = 0.01 (1% per month)

The amortisation schedule shows exactly how each EMI is split between interest and principal - month by month. This is the most powerful tool for understanding your loan.

In Month 1, ₹5,000 of your ₹16,607 EMI is pure interest - 30% of your payment goes to the bank before you reduce the principal by even ₹1.

By Month 36, only ₹164 is interest - almost your entire last EMI is principal repayment.

This is why prepayments made early in the loan tenure are so much more valuable than prepayments made later.

In Month 3, a ₹50,000 prepayment reduces ₹50,000 of principal and eliminates interest on that ₹50,000 for all remaining months. In Month 30, the same prepayment saves very little because the principal is already low.

How Interest Rate Affects Your Total Cost - Side-by-Side

Interest Rate

Monthly EMI (₹5L, 36M)

Total Interest

Total Outgo

9.99%

₹16,134

₹80,824

₹5,80,824

12%

₹16,607

₹97,852

₹5,97,852

14%

₹17,087

₹1,15,132

₹6,15,132

16%

₹17,577

₹1,32,772

₹6,32,772

18%

₹18,076

₹1,50,736

₹6,50,736

The difference between getting 9.99% and 18% on the same ₹5 lakh loan over 3 years is ₹69,912 in total interest. That is nearly 14% of the principal, entirely determined by your CIBIL score and lender choice.

This is why checking your CIBIL score before applying - and comparing lenders directly helps in saving your money.

How Tenure Affects Your Total Cost

Tenure

EMI (₹5L, 12%)

Total Interest

Difference vs 12 Months

12 months

₹44,424

₹33,088

Baseline

24 months

₹23,536

₹64,864

₹31,776

36 months

₹16,607

₹97,852

₹64,764

60 months

₹11,122

₹1,67,320

₹1,34,232

Choosing 60 months instead of 12 months saves ₹33,302 per month in EMI - but costs you ₹1,34,232 more in total interest. That is 26.8% of the original loan amount just in extra interest for the privilege of lower monthly payments.

Smart strategy: Choose the shortest tenure your FOIR (debt-to-income ratio) can comfortably support. Then make prepayments aggressively when surplus funds are available - with zero penalty on floating rate loans in 2026.

Flat Rate to Reducing Balance Conversion

Many NBFCs and some fintech lenders still advertise flat rates. If your lender quotes a flat rate, convert it to the effective reducing balance rate before comparing:

Rule of thumb: A flat rate of X% is approximately equivalent to a reducing balance rate of 1.7X to 1.9X%.

Example: Flat rate of 7% → Effective reducing balance rate ≈ 12% to 13%

Always ask your lender: "Is this a flat rate or a reducing balance rate?" before signing the agreement.

APR vs Interest Rate - The Hidden Extra Cost

The interest rate your lender advertises does not include processing fees. The APR (Annual Percentage Rate) does -, and it is always higher.

Example

₹5 lakh loan at 12% interest rate

Processing fee 2% = ₹10,000 deducted upfront

You receive ₹4,90,000 but repay as if you borrowed ₹5,00,000

Effective APR = approximately 13.8%

APR of personal loans usually ranges between 11.29% to 35%.

Under RBI's Digital Lending Directions 2025, all lenders must disclose APR in the Key Fact Statement (KFS). Always compare APR across lenders - not just the headline interest rate.

How to Reduce Your Personal Loan Interest Cost?

The following are 4 most important and practical tips to reduce your personal loan interest cost:

Improve your CIBIL score before applying. The difference between 9.99% and 14% on a ₹5 lakh 3-year loan is ₹34,308 in total interest. A 750+ score unlocks the best rates.

Choose the shortest tenure your income supports. As the table above shows, 12 months vs 60 months on ₹5 lakh saves ₹1,34,232 in interest.

Prepay aggressively in the first half of the tenure. The amortisation schedule shows that the early months carry the highest interest component. Every ₹10,000 prepaid in Month 3 saves more interest than the same amount prepaid in Month 30.

Compare APR, not just interest rate. A loan at 11% with 3% processing fee may cost more than a loan at 12% with 0.5% processing fee. Always compare the full-cost APR using a loan calculator.

Summary

Understanding personal loan interest calculation puts you in control of one of the most important financial decisions you will make. Here is the complete recap:

The formula: EMI = P × R × (1 + R)^N ÷ [(1 + R)^N − 1] P = Principal, R = Monthly rate (annual ÷ 12 ÷ 100), N = Tenure in months.

Example: ₹5 lakh at 12% for 36 months → EMI = ₹16,607, Total interest = ₹97,852.

Reducing balance vs flat rate: Always use reducing balance. Flat rate on the same loan costs ₹82,148 more.

Tenure impact: Longer tenure = lower EMI, dramatically higher total interest. Choose the shortest tenure your budget supports.

Rate impact: 9.99% vs 18% on ₹5 lakh for 3 years = ₹70,000 difference in total interest.

APR matters more than interest rate: Processing fees make the effective cost higher than the headline rate.

How do I calculate a personal loan interest rate manually?

Use the EMI formula: EMI = P × R × (1+R)^N ÷ [(1+R)^N − 1], where P is the loan amount, R is the monthly interest rate (annual rate ÷ 12 ÷ 100), and N is the number of months - then multiply EMI by N and subtract P to get the total interest.

What is the difference between flat rate and reducing balance?

Most personal loans in India use the reducing balance method, where interest is recalculated on the outstanding principal after each payment - flat-rate loans appear cheaper but cost significantly more overall.

How to calculate SBI personal loan EMI?

SBI personal loans use the reducing balance method; use the formula above with SBI's current rate (starting from 10% p.a.) and your preferred tenure, or use the official SBI free EMI calculator

How much total interest do I pay on ₹10 lakh at 12% for 5 years?

At 12% per annum for 60 months: EMI = ₹22,244, total repayment = ₹22,244 × 60 = ₹13,34,640, total interest = ₹13,34,640 − ₹10,00,000 = ₹3,34,640.

What is APR, and why is it different from the interest rate?

APR (Annual Percentage Rate) includes the interest rate plus all fees like processing charges - it is always higher than the headline interest rate and represents the true annual cost of borrowing; the APR of personal loans usually ranges from 11.29% to 35%.

How does prepayment reduce my interest cost?

Prepayment reduces your outstanding principal immediately - since interest is calculated on the reducing balance, a lower principal means less interest in all future months; prepayments made in the early months of the loan save the most because that is when the interest component of each EMI is highest.

Sources

Axis Bank - Personal Loan EMI Calculator and Formula: axis.bank.in/calculators/personal-loan-emi-calculator

HDFC Bank - Personal Loan EMI Calculator: hdfc.bank.in/personal-loan/emi-calculator

ICICI Bank - Personal Loan Interest Rates and EMI Calculator (Q1 2026): icici.bank.in/personal-banking/loans/personal-loan

Bajaj Finance - Personal Loan EMI Calculator and Rates: bajajfinserv.in/personal-loan-emi-calculator

Paisabazaar - Personal Loan Interest Rates (May–June 2026): paisabazaar.com/personal-loan/interest-rates

RBI - Key Fact Statement Requirements under Digital Lending Directions 2025: rbi.org.in

InvestKraft - Personal Loan EMI Calculator: investkraft.com

Disclaimer: EMI calculations in this article are indicative and based on the reducing balance method. Actual EMI may vary based on lender-specific calculation methods, processing fees, and rounding. Always verify with your lender's official calculator before finalising any loan. This article is for informational purposes only.

Author: Diwakar Kumar Singh

Diwakar Kumar Singh is a BFSI specialist and finance writer with over 7 years of hands-on experience in financial research, content creation, and analysis.

A Gold Medalist in MBA (Marketing) from IMT, he combines deep analytical skills with practical insights gained from evaluating companies, IPOs, unlisted shares, financial ratios, and investment opportunities. Diwakar has personally analysed hundreds of financial instruments and market scenarios, which he uses to break down complex topics into clear, actionable advice.

He has authored numerous in-depth finance articles, published multiple books internationally, and contributed to research publications. His work focuses on helping everyday investors and readers make better-informed financial decisions through well-researched, evidence-based explanations that are always grounded in real-world application rather than theory alone.